UK State Pension Living in Australia: The Voluntary National Insurance Hack

British expats living in Australia can still claim the UK new state pension. Learn how making voluntary National Insurance contributions boosts your retirement.

British expats living in Australia can still claim the UK new state pension. Learn how making voluntary National Insurance contributions boosts your retirement.

Stop wasting time on academic textbooks. These are the best personal finance and investing books that will actually change how you manage your money.

A tiny 1% fee can steal 20% of your retirement nest egg. Use my free investment fee calculator to see how much you are losing to managed fund fees.

Australians pay double the superannuation fees of other Western nations, costing me $20 billion a year. See how much these fees cost Dave the plumber.

When you start living off your assets, every sell order is a potential tax event. Here is how to sequence your sales to minimise Capital Gains Tax in Australia.

Most Australians pay a hidden "tax drag" inside their super every year. Here is how switching to a direct investment option can legally wipe your CGT at retirement.

Setting up a share portfolio for your kids is a brilliant idea, but the ATO has some nasty traps. Here's how to use informal trusts and growth ETFs to invest tax-free.

Before you click 'Buy' on your next ETF, make sure you run through this simple checklist. Missing just one of these factors could cost you thousands in UK tax and FX fees.

Living overseas but still holding UK shares? Watch out. The UK inheritance tax rules for non-residents mean your estate could face a surprise 40% tax bill.

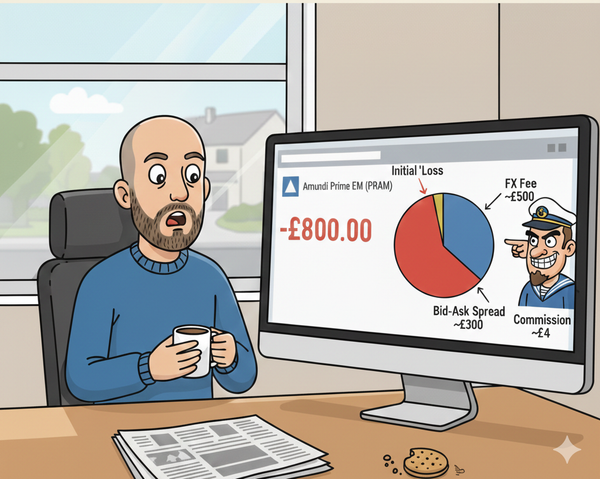

Hit 'Buy' on an international share only to see your balance instantly drop? Discover the hidden FX fees and spreads that are draining your wallet.

Ever wondered what the "index" in index funds actually means? Here is a simple, jargon-free breakdown of how index funds work and the main market benchmarks.

Want the lowest fees on your super? I compare the cheapest 100% equity and growth index super options in Australia from Hostplus, AustralianSuper, and Vanguard.

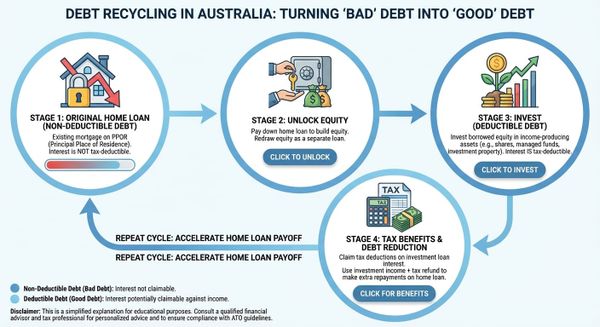

Want to make your mortgage interest tax-deductible? Here is how the debt recycling strategy works in Australia, straight from the ATO rulebook.

No intro rates, no annoying conditions, no jumping through hoops. I compare the best high interest savings accounts in Australia to find a genuine home for your cash.

Thinking about hosting your home on Airbnb while on holiday? Before you list, learn how platforms fees, local NSW STRA regulations, and the ATO's CGT rules can eat your profit.

Looking at a friend's UK pension fund fees revealed a shocking truth: high active management fees and platform charges can steal over half your pot. Here's why.